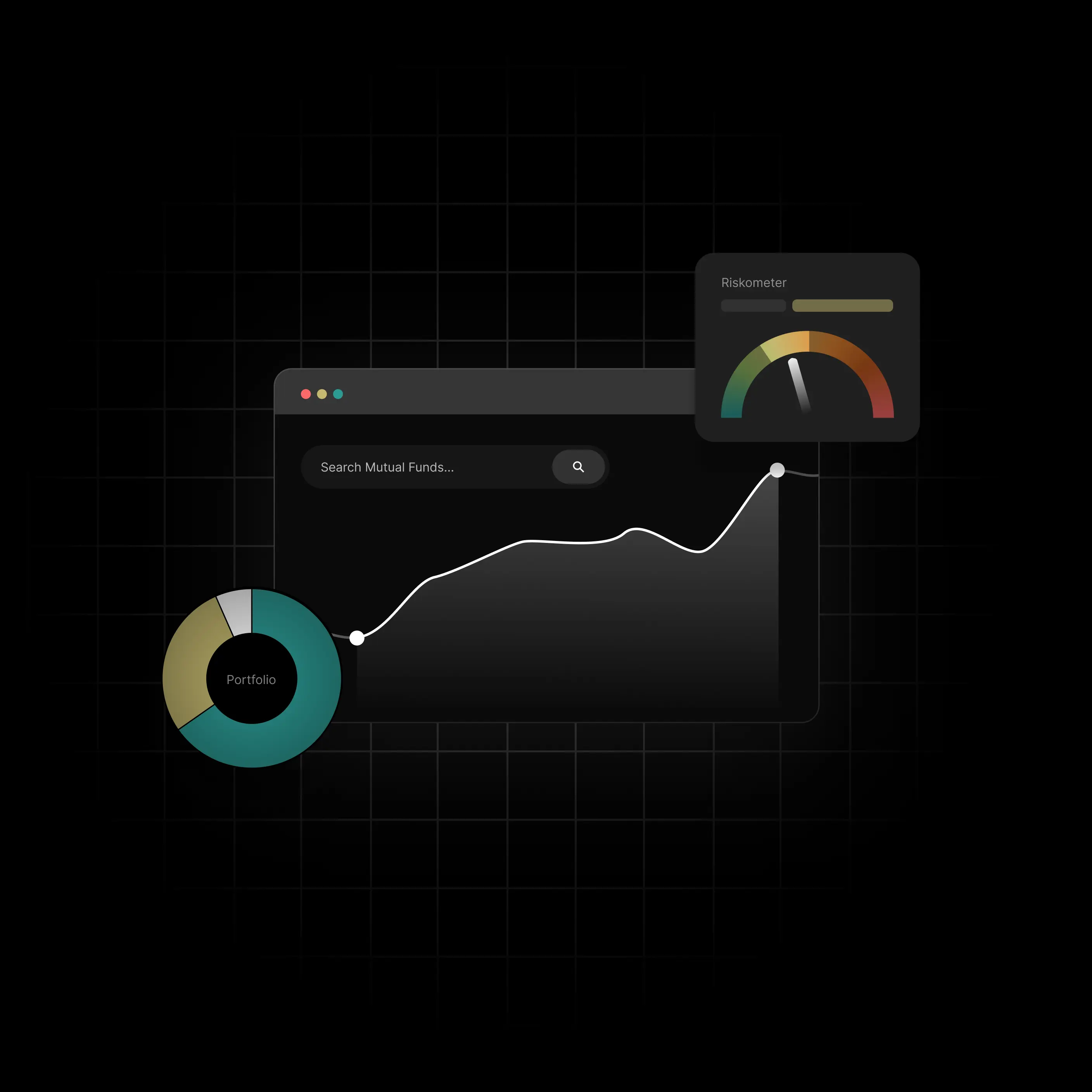

Discover

Mutual Funds

Explore the world of mutual funds that can help you achieve financial goals and create wealth.

LEARN ABOUT MUTUAL FUNDS

What are Mutual Funds?

Mutual Funds pool or collect money from a large number of investors. This money is invested in securities like equity, debt, and commodities by professional fund manager(s) and their team.

Types of Mutual Funds

Equity Funds

Equity funds mainly invest in stocks of different companies, making investors partial owners of those companies when they invest in such funds.

Debt Funds

Debt Mutual Funds invest in fixed-income securities such as government bonds, corporate bonds, treasury bills, and other money market instruments.

Hybrid Funds

Hybrid funds are a combination of equity and debt investments. The blend of these asset classes varies based on the fund's investment goals.

Best Mutual Funds Across Categories

Sort By

| Fund name | Fund size | Expense Ratio | 3Y Returns |

|---|---|---|---|

SBI Bluechip Fund Direct Growth Large-Cap Very High Risk | ₹55,063 Cr | 0.79% | 10.8% |

SBI Small Cap Fund Direct Growth Small-Cap Very High Risk | ₹40,156 Cr | 0.74% | 14.0% |

Nippon India Small Cap Fund Direct Growth Small-Cap Very High Risk | ₹78,407 Cr | 0.54% | 18.8% |

Canara Robeco Small Cap Fund Direct Growth Small-Cap Very High Risk | ₹13,967 Cr | 0.46% | 15.5% |

Mirae Asset Emerging Bluechip Direct Growth Large & Mid-Cap Very High Risk | ₹42,792 Cr | 0.49% | 15.4% |

Axis Bluechip Fund Direct Growth Large-Cap Very High Risk | ₹30,004 Cr | 0.75% | 9.7% |

Axis Midcap Fund Direct Growth Mid-Cap Very High Risk | ₹32,852 Cr | 0.57% | 18.5% |

Axis Long Term Equity Fund Direct Growth ELSS (Tax Savings) Very High Risk | ₹31,023 Cr | 0.87% | 11.3% |

Axis Small Cap Fund Direct Growth Small-Cap Very High Risk | ₹27,840 Cr | 0.61% | 17.4% |

Parag Parikh Flexi Cap Fund Direct Growth Flexi Cap Very High Risk | ₹1,43,388 Cr | 0.53% | 15.1% |

Take control of your wealth

Download the App

MUTUAL FUND BASKETS

Expert backed portfolios, personalised for you.

Get an expert managed Mutual Fund basket with periodic rebalancing and beat the benchmark!

Multi Asset - Conservative

Multi Asset - Conservative

Prioritising safety over high returns.

Returns (10Yr)

8.1% p.a

Ideal holding

2+ years

Volatility

Low

Portfolio type

Equity + Debt

Multi Asset - Growth

Multi Asset - Growth

Focused on higher returns while minimising risk.

Returns (10Yr)

13.4% p.a

Ideal holding

3+ years

Volatility

Medium

Portfolio type

Equity + Debt

Equity - Growth

Equity - Growth

High-risk approach to maximize returns over the long-term.

Returns (10Yr)

16.5% p.a

Ideal holding

5+ years

Volatility

High

Portfolio type

Equity

From a team that has done it before.

Meet experts with decades of investing experience

₹50,000Cr

Previously managed

20Years

Of Expertise

Backed by leading investors:

Our Investment Team

Investment

Pratik Bagaria

Ex Motilal Oswal

MBA

Investment

Ravi Ajmera

Ex Hero FinCorp.

CFA, Msc

Investment

Kumar Jain

Ex Motilal Oswal

CFA, PDDBM

Investment

Hardik Shah

Ex Karza Technologies

MMS

Do you invest in mutual funds?

We're dedicated to aiding you in achieving a seamlessly navigable investment environment.

Get your investments reviewed

Identify red flags in your portfolio and gain actionable insights to increase your returns.

Advantages of Mutual Funds

Investing in mutual funds can help you in multiple ways. A few use cases of bonds are discussed below:

Managed by Professional Fund Managers

Dozens of Types, Thousands of Schemes

Require Low Effort from Investors

Offer In-built Diversification that Lowers Risk

Mutual Fund Investment Methods

Systematic Investment Plan

Starting an SIP is super easy. All you have to do is select mutual fund schemes, define a date for monthly debit and investment amount and to start the SIP.

SIP offers the convenience of automatic monthly investing with the benefit of reducing market volatility through rupee cost-averaging.

Lumpsum Investment

Lumpsum mutual fund investments refers to investing substantial sums of money in a mutual fund scheme(s) in one go.

Lumpsum investments are considered to be riskier than SIP because you invest the entire sum in one go instead of spreading it over time. But lumpsum investments also have the potential to generate higher returns than SIP if timed right

How to Invest in Mutual Funds Online?

Get started

Get started by answering a few questions and choosing an investment option

Make Investment

Start an SIP or invest a lumpsum amount or better, start both!

Review & Approve

Review and approve regular rebalancing updates as your wealth grows

Mutual Fund Basic Concepts

Net Asset Value (NAV)

Systematic Investment Plan (SIP)

Total Expense Ratio (TER)

All About Mutual Funds

How Do Mutual Funds Work?

Mutual Funds pool or collect money from a large number of investors. This money is invested in securities like equity, debt and commodities by professional fund manager(s) and their team.

When you invest in a mutual fund scheme, you receive units of the scheme. The price of each mutual fund unit is referred to as NAV (Net Asset Value). As the value of the underlying securities increases, the NAV increases and so does the value of your investment in the scheme.

Whenever you need your invested money back, you can place a ‘redemption’ order. This means that you will sell your units and receive a credit amount depending on the number of units you sell, the prevailing NAV, and exit load, if applicable.

Benefits of Investing in Mutual Funds

Managed by Professional Fund Managers

Mutual fund schemes are managed by fund managers who have vast experience in the financial markets.

More often than not, the fund managers have educational qualifications like CA (Chartered Accountant), CFA (Chartered Financial Analyst), MBA (Masters in Business Administration).

Dozens of Types, Thousands of Schemes

Mutual funds don’t have a dearth of options. Firstly, close to 50 AMCs (Asset Management Companies) offer mutual fund schemes in India.

Next, mutual funds are categorised as per the asset class they invest in - equity, debt, or hybrid. Each mutual fund category has several types. For example - large-cap mutual funds are a type of equity mutual funds.

Because of this, over 1,000 mutual fund schemes are available for investing in India. Source - AMFI

Require Low Effort from Investors

Mutual funds are simple instruments for investors.

Most critical investment decisions associated with asset allocation, market cap allocation, buying and selling securities etc. are taken by the fund’s management teams. These decisions don’t require your review or approval or even in-depth understanding.

All you need to do is invest in the fund and the rest of it is taken care of by professionals.

Offer In-built Diversification that Lowers Risk

Diversification refers to spreading out your money across different assets (like equity, debt etc.) and across different securities (like stocks, bonds, etc.).

Mutual funds are diversified by design. By investing in a single equity mutual fund scheme, you get exposure to dozens of stocks.

Diversification helps in lowering investment risk. Think about it - if you invest in stocks of just one company, it is possible that the company can go bankrupt, wiping out your entire investment. But if you invest in stocks of many different companies, your money is not entirely at risk.

Accessible and Affordable Investing

Anyone can invest in mutual funds. All you need is a smartphone, Rs. 500 in your bank account and 5 minutes to invest in mutual funds, making them super accessible.

Mutual funds charge their investors in proportion of their investments. The charges are also referred to as expense ratios and are generally in the 1-2% range depending on the mutual fund scheme.

Get Your Money Back When You Want it

Most mutual funds are open-ended, meaning you can invest in them and withdraw your investments whenever you want. So you can easily access your mutual fund investments during times of need.

It is important to note that withdrawal may have adverse implications on the returns you will generate, taxes you will pay and may attract exit load.

It is important to note that units of close-ended mutual fund schemes can be redeemed only on maturity. And, units of ELSS have a 3-year lock-in period and can be liquidated only thereafter

Tightly Regulated by the SEBI

Mutual Funds are regulated by the capital markets regulator, Securities and Exchange Board of India (SEBI) under SEBI (Mutual Funds) Regulations, 1996.

The regulations and guidelines protect the investors from various activities of mutual funds - advertising, distributing, pricing, managing portfolio risks etc.

More Favourable Taxation than Direct Stock Investing

You can get equity exposure either by investing in equity mutual funds or direct stocks. While one may work better than the other from a returns perspective, equity mutual funds have more favourable taxation.

When you invest in direct stocks, you have to pay taxes whenever you sell your stocks at a profit or receive dividends. However, when mutual funds do it for you, they are not taxed. The taxation incidence occurs only when you sell the mutual fund units at a profit. Thus, mutual funds enjoy uninterrupted compounding that works in your favour.

Best ways to invest in Mutual Funds Online

If you have heard of mutual funds, you have heard of SIPs or Systematic Investment Plans. SIP is one of the two mutual fund investment methods, the other being lumpsum.

Systematic Investment Plan

Starting an SIP is super easy. All you have to do is select mutual fund schemes, define a date for monthly debit and investment amount and to start the SIP.

SIP offers the convenience of automatic monthly investing with the benefit of beating market volatility through rupee cost-averaging. However, please remember that the Rupee cost averaging does not assure a profit, nor does it protect one against investment losses in declining markets.

Lumpsum Investment

Lumpsum mutual fund investments refers to investing substantial sums of money in a mutual fund scheme(s) in one go.

Lumpsum investments are considered to be riskier than SIP because you invest the entire sum in one go instead of spreading it over time. But lumpsum investments also have the potential to generate higher returns than SIP if timed right.

Types of Mutual Funds Schemes

Mutual funds can be categorised into different types depending on various factors. For example: Investment objective can be a factor and there can be 3 types based on it - Growth, Income and Liquidity.

But the most intuitive way to categorise mutual funds is based on the asset classes they take exposure to or their portfolio composition. Based on this and to for the sake of simplicity, we can say that there are 3 types of mutual funds:

- Equity Mutual Funds

- Debt Mutual Funds

- Hybrid Mutual Funds

Equity Mutual Funds

Equity mutual funds invest most of their assets in equity and related instruments.

In a growing economy like India, equity offers high growth potential but the risk of investing in equity is also relatively higher.

Some popular types of equity mutual funds are - large-cap funds, mid-cap funds, small-cap funds, ELSS (Equity Linked Savings Schemes) funds, and flexi-cap funds.

Debt Mutual Funds

Debt mutual funds invest most of their assets in debt instruments. Since debt instruments are lower risk than equity, debt funds are lower risk than equity funds.

Debt funds offer features like income generation, stable returns, high liquidity, and reasonable safety.

Some popular types of debt mutual funds are - liquid funds, money market funds, corporate bond funds, and dynamic bond funds.

Hybrid Mutual Funds

Hybrid mutual funds typically invest in a mix of debt and equity instruments. So, investors can benefit from the stability offered by debt and the growth offered by equity through a single hybrid fund.

Some popular types of hybrid funds are - balanced advantage funds, aggressive hybrid funds, multi-asset allocation funds, and arbitrage funds.

All About Mutual Funds

How Do Mutual Funds Work?

Mutual Funds pool or collect money from a large number of investors. This money is invested in securities like equity, debt and commodities by professional fund manager(s) and their team.

When you invest in a mutual fund scheme, you receive units of the scheme. The price of each mutual fund unit is referred to as NAV (Net Asset Value). As the value of the underlying securities increases, the NAV increases and so does the value of your investment in the scheme.

Whenever you need your invested money back, you can place a ‘redemption’ order. This means that you will sell your units and receive a credit amount depending on the number of units you sell, the prevailing NAV, and exit load, if applicable.

Benefits of Investing in Mutual Funds

Managed by Professional Fund Managers

Mutual fund schemes are managed by fund managers who have vast experience in the financial markets.

More often than not, the fund managers have educational qualifications like CA (Chartered Accountant), CFA (Chartered Financial Analyst), MBA (Masters in Business Administration).

Dozens of Types, Thousands of Schemes

Mutual funds don’t have a dearth of options. Firstly, close to 50 AMCs (Asset Management Companies) offer mutual fund schemes in India.

Next, mutual funds are categorised as per the asset class they invest in - equity, debt, or hybrid. Each mutual fund category has several types. For example - large-cap mutual funds are a type of equity mutual funds.

Because of this, over 1,000 mutual fund schemes are available for investing in India. Source - AMFI

Require Low Effort from Investors

Mutual funds are simple instruments for investors.

Most critical investment decisions associated with asset allocation, market cap allocation, buying and selling securities etc. are taken by the fund’s management teams. These decisions don’t require your review or approval or even in-depth understanding.

All you need to do is invest in the fund and the rest of it is taken care of by professionals.

Offer In-built Diversification that Lowers Risk

Diversification refers to spreading out your money across different assets (like equity, debt etc.) and across different securities (like stocks, bonds, etc.).

Mutual funds are diversified by design. By investing in a single equity mutual fund scheme, you get exposure to dozens of stocks.

Diversification helps in lowering investment risk. Think about it - if you invest in stocks of just one company, it is possible that the company can go bankrupt, wiping out your entire investment. But if you invest in stocks of many different companies, your money is not entirely at risk.

Accessible and Affordable Investing

Anyone can invest in mutual funds. All you need is a smartphone, Rs. 500 in your bank account and 5 minutes to invest in mutual funds, making them super accessible.

Mutual funds charge their investors in proportion of their investments. The charges are also referred to as expense ratios and are generally in the 1-2% range depending on the mutual fund scheme.

Get Your Money Back When You Want it

Most mutual funds are open-ended, meaning you can invest in them and withdraw your investments whenever you want. So you can easily access your mutual fund investments during times of need.

It is important to note that withdrawal may have adverse implications on the returns you will generate, taxes you will pay and may attract exit load.

It is important to note that units of close-ended mutual fund schemes can be redeemed only on maturity. And, units of ELSS have a 3-year lock-in period and can be liquidated only thereafter

Tightly Regulated by the SEBI

Mutual Funds are regulated by the capital markets regulator, Securities and Exchange Board of India (SEBI) under SEBI (Mutual Funds) Regulations, 1996.

The regulations and guidelines protect the investors from various activities of mutual funds - advertising, distributing, pricing, managing portfolio risks etc.

More Favourable Taxation than Direct Stock Investing

You can get equity exposure either by investing in equity mutual funds or direct stocks. While one may work better than the other from a returns perspective, equity mutual funds have more favourable taxation.

When you invest in direct stocks, you have to pay taxes whenever you sell your stocks at a profit or receive dividends. However, when mutual funds do it for you, they are not taxed. The taxation incidence occurs only when you sell the mutual fund units at a profit. Thus, mutual funds enjoy uninterrupted compounding that works in your favour.

Best ways to invest in Mutual Funds Online

If you have heard of mutual funds, you have heard of SIPs or Systematic Investment Plans. SIP is one of the two mutual fund investment methods, the other being lumpsum.

Systematic Investment Plan

Starting an SIP is super easy. All you have to do is select mutual fund schemes, define a date for monthly debit and investment amount and to start the SIP.

SIP offers the convenience of automatic monthly investing with the benefit of beating market volatility through rupee cost-averaging. However, please remember that the Rupee cost averaging does not assure a profit, nor does it protect one against investment losses in declining markets.

Lumpsum Investment

Lumpsum mutual fund investments refers to investing substantial sums of money in a mutual fund scheme(s) in one go.

Lumpsum investments are considered to be riskier than SIP because you invest the entire sum in one go instead of spreading it over time. But lumpsum investments also have the potential to generate higher returns than SIP if timed right.

Types of Mutual Funds Schemes

Mutual funds can be categorised into different types depending on various factors. For example: Investment objective can be a factor and there can be 3 types based on it - Growth, Income and Liquidity.

But the most intuitive way to categorise mutual funds is based on the asset classes they take exposure to or their portfolio composition. Based on this and to for the sake of simplicity, we can say that there are 3 types of mutual funds:

- Equity Mutual Funds

- Debt Mutual Funds

- Hybrid Mutual Funds

Equity Mutual Funds

Equity mutual funds invest most of their assets in equity and related instruments.

In a growing economy like India, equity offers high growth potential but the risk of investing in equity is also relatively higher.

Some popular types of equity mutual funds are - large-cap funds, mid-cap funds, small-cap funds, ELSS (Equity Linked Savings Schemes) funds, and flexi-cap funds.

Debt Mutual Funds

Debt mutual funds invest most of their assets in debt instruments. Since debt instruments are lower risk than equity, debt funds are lower risk than equity funds.

Debt funds offer features like income generation, stable returns, high liquidity, and reasonable safety.

Some popular types of debt mutual funds are - liquid funds, money market funds, corporate bond funds, and dynamic bond funds.

Hybrid Mutual Funds

Hybrid mutual funds typically invest in a mix of debt and equity instruments. So, investors can benefit from the stability offered by debt and the growth offered by equity through a single hybrid fund.

Some popular types of hybrid funds are - balanced advantage funds, aggressive hybrid funds, multi-asset allocation funds, and arbitrage funds.

Related Articles

Still got questions? We’re here to help.

What is a mutual fund, and how does it work?

Mutual funds are professionally managed instruments that pool or collect money from many investors and invest it in securities like stocks and bonds. Each mutual fund scheme has a well-defined mandate and the scheme is required to follow it while investing in securities.

What are the different types of mutual funds available in India?

There are 5 mutual fund categories in India.

- Equity mutual funds

- Debt mutual funds

- Hybrid mutual funds

- Solution-oriented funds

- Other funds

Each of the above categories has multiple sub-categories. For example - large-cap funds are a sub-category under the equity mutual funds category.

What is the minimum investment required to start investing in mutual funds?

One of the best features of mutual funds is the very low investment required to invest in them. While the amount may differ for different schemes, it is in the range of Rs. 100 to Rs. 5,000.

How can I choose the right mutual fund for my investment goals and risk tolerance?

While the internet is rife with ‘best mutual funds,’ the right mutual fund is different for every individual. A holistic understanding of your investment objectives, risk profile and other aspects is necessary before shortlisting mutual funds for investment. A financial advisor is best placed to do this for you.

How often should I review my mutual fund portfolio?

While the review process and frequency depend on the objective and construction of the portfolio, it is recommended that diversified mutual fund portfolios be reviewed once a year at least.

What is the expense ratio, and how does it impact my returns?

The expense ratio is the industry term for fees charged by mutual funds for managing and investing your money. The expense ratio is expressed as a percentage (for example: 1%) and indicates the annual fee a mutual fund scheme will charge you as a percentage of your investment.

Are there any penalties or charges for early withdrawal or redemption of mutual fund units?

Yes, many mutual funds (especially equity funds) have exit load applicable for early exit (typically within 1 year of investment). The exit load varies across funds but is 1% for most equity funds.

Are there any tax implications associated with investing in mutual funds?

Yes, mutual funds attract taxation on the capital gains they generate for you. The taxation is applicable on realized (booked) gains and not on notional gains. As of 2023, there are 3 types of taxation applicable on mutual funds depending on their domestic equity allocation: less than 35%, 35-65%, more than 65%.

If domestic equity allocation is less than 35% (examples - debt funds, international equity funds), capital gains are taxed at your marginal income tax rate, irrespective of the holding period.

If domestic equity allocation is 35-65% (examples - certain hybrid funds), short term capital gains (less than 3 years) are taxed at your marginal income tax rate. If the capital gains are more than 3 years old (long term capital gains), then the taxation is flat 20% with the benefit of indexation.

If domestic equity allocation is more than 65% (examples - equity funds), short term capital gains (less than 1 year) are taxed at flat 15%. If the capital gains are more than 1 year (long-term capital gains), then the taxation is flat 10% for capital gains in excess of Rs. 1 lakh

How can I track the performance of my mutual fund investments?

You can analyse as well as track your mutual fund portfolio on the Dezerv Wealth Monitor app. Download the Dezerv Wealth Monitor here.

What is the difference between growth and IDCW options in a mutual fund?

Growth mutual fund schemes don’t return your money until you place a withdrawal or redemption order. All the profits and income generated by the underlying stocks and bonds in the form of dividends and interest are reinvested into the scheme.

IDCW or Income Distribution cum Capital Withdrawal schemes pay out the income they generate to investors at their discretion.

Most mutual fund schemes offer growth as well as IDCW options. Learn more about IDCW vs Growth

What are the methods of investing in mutual funds?

You can invest in mutual fund schemes of your choice in one of two ways: SIP or lumpsum.

SIP or Systematic Investment Plan refers to investing a fixed amount in a mutual fund scheme regularly (mostly monthly). A SIP needs to be set up just once, and your money gets invested as per the rule of the SIP automatically until you cancel it.

Lumpsum investment method refers to making a non-recurring, one-time investment in a mutual fund scheme.

Are there any regulatory bodies overseeing mutual funds in India, and how are they regulated?

The SEBI (Securities Exchange Board of India) is the regulatory body for all entities associated with stocks, bonds and the capital market in general. The SEBI also regulates mutual funds in India with the objective of protecting mutual fund investors.

Track & Analyse all your investments in one place

Compare your portfolio's performance with benchmarks

Identify potential risks in your portfolio and learn to fix them

Track all your family's investments in one place

Trending Mutual Funds Searches

Popular Equity Funds

Popular Debt Funds

Dezerv Investments Pvt. Ltd. is a Portfolio Manager with SEBI Registration no. INP000007377. Distribution services are offered through Dezerv Distribution Services Pvt. Ltd. (APRN 00615). Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Performance data of Portfolio Manager and Investment Approach provided hereunder is not verified by SEBI. Terms and conditions of the website are applicable.Privacy Policy of the website is applicable.