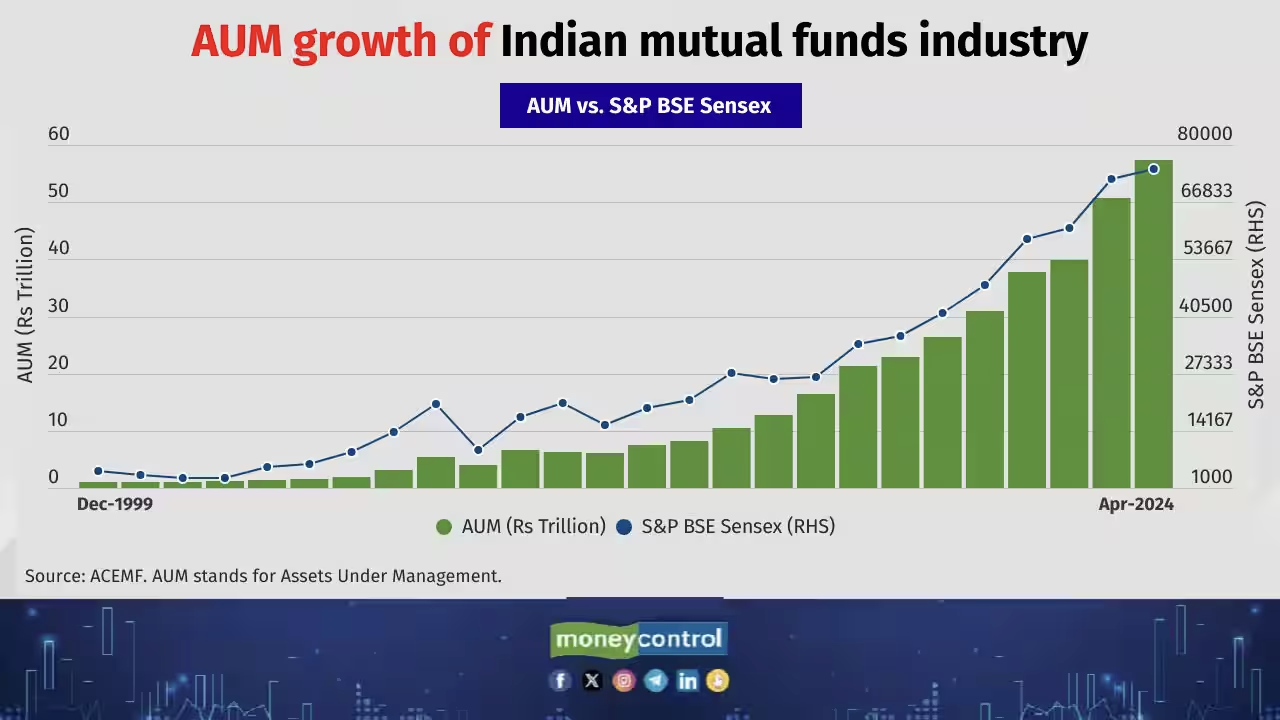

To say the Indian mutual fund industry is growing would be an understatement.

The total assets under management (AUM) were at about ₹24.25 trillion in June 2019. Five years later, and the AUM has more than doubled! It reached ₹61.16 trillion on June 30, 2024!

Source: Moneycontrol

So, the real question is, what’s fuelling this growth?

Is India taking to investing in mutual funds like never before? Do we suddenly have a lot more surplus funds?

Wouldn’t THAT be ideal?

No, one of the most significant reasons for this evolution is the impact of technology. Or rather, fintech.

Let’s take a look at how fintech has evolved and changed the mutual fund distribution process as we know it.

Before Fintech

Well, there are about a hundred or so ways in which fintech and the evolution of technology have changed the face of the mutual fund industry.

But it comes down to two main things:

- Convenience

- Awareness

Let’s take a moment to reflect on why someone would choose to NOT invest in mutual funds.

Scenario 1:

Arun has a basic understanding of the stock market and other forms of investment. He is aware of the importance of creating a portfolio for oneself, especially for the long term.

Arun has been saving a fixed amount from his monthly salary. But sadly, these funds don’t get to travel much further than his savings account.

His friends keep telling him to invest that money, to generate some returns for himself. He wants to do it. It’s just that he’s so busy at work, that he is not getting the time to do so.

Plus, he’s a little intimidated by the entire investment space, and he doesn’t know where to start. So many forms, so many documents — who has the time?

Scenario 2:

Arun has no idea where to invest his money. He believes that the stock market is akin to gambling, and he feels it will be safer to either keep his money in his savings account, or at most, set up a recurring deposit.

The world of mutual fund investments is not even in his orbit.

The growth of technology in the investment space has targeted these two root problems.

First, the convenience factor.

Gone are the days when you would have to go down to the AMC office and sift through a mountain of paperwork to start your investment. Now, you can do so in a few minutes from the comfort of your own home.

Second is the awareness factor.

This is something that both the regulatory bodies in India as well as the individual fund houses and investment platforms have been working on tirelessly.

From television ads on Mutual Fund Sahi Hai to social media campaigns on the various benefits of investing in mutual funds — we have seen it all.

Source: Mutual Funds Sahi Hai

And it has been working!

From 19 million investors in 2018 to over 40 million in 2024, we have certainly come a long way. It’s certainly impressive.

But there’s still a lot more to go. 40 million in a country with a population of 1.4 billion comes up to less than 3%!

“The main objective we want to work towards is financial inclusion because we think the penetration level at this time is still limited with just 40 million unique PAN folios in a population of 1.4 billion.” — Vishal Jain, CEO, Zerodha Mutual Fund

After Fintech

Let’s take a look at some of the key innovations that fintech has brought into the mutual fund industry.

- Digital Onboarding and KYC (Know Your Customer)

Fintech has done away with paperwork and brought the onboarding process to your screens. Investors can now complete their KYC formalities online within minutes using Aadhaar-based verification, e-signatures and video KYC.

- Online Investment Platforms

New-age investment platforms offer investors the ability to purchase and manage mutual fund investments entirely online. They focus on user-friendly interfaces and provide comprehensive information on various funds.

Plus, you can even use tools like Dezerv’s Wealth Monitor to compare performance and see how your portfolio is doing.

- Automated Investments

One of the main pain points that have held people back is the manual investment process. With SIPs and other forms of automated investments, this is no longer a concern.

Let’s Talk Numbers

- Increased Retail Participation

According to AMFI, there are currently about 19.10 crore investor accounts as of June 2024. Out of these the majority of these are retail investors.

Source: Moneycontrol

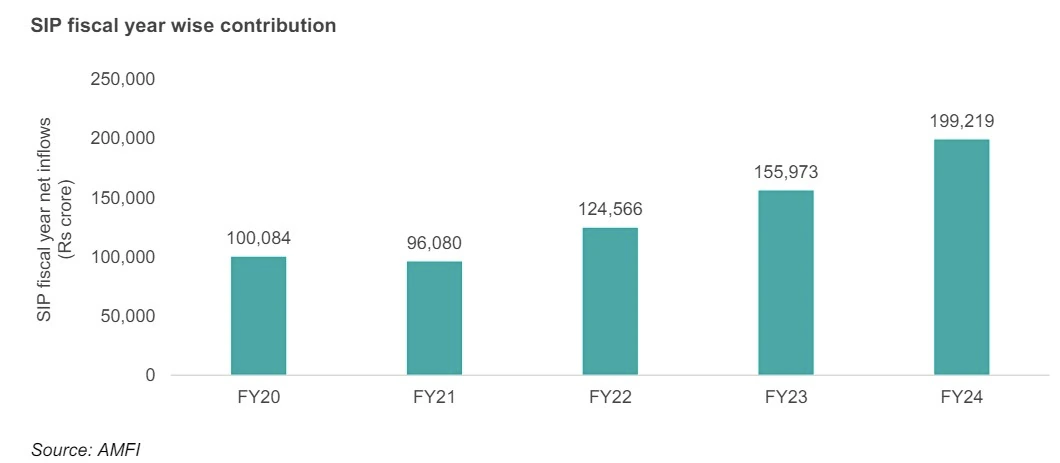

- Growth in SIPs

According to AMFI data, the number of SIP accounts has been increasing steadily and reached 8.76 crores. In May 2024 alone, a total of ₹20,904 crores was invested.

Source: Business Today

- Digital Transactions

In the last ten years or so, the share of digital transactions in total payments has been increasing steadily. Data from IBEF shows that the share of digital payments has increased from 1% to 21%!

This, of course, is driven by the new-age investors and the ever-growing popularity of UPI.

The Road Ahead

The question is, what does this mean for investors and advisors?

For investors, the road is just going to get easier. This is just the tip of the iceberg. As more and more innovations start coming up in fintech, the process of investing in mutual funds will become simpler.

As for advisors and distributors, it opens up a whole new demographic. If you consider how under-penetrated the Indian markets still are, it will show exactly how huge the opportunity is. And advisors can tap right into this.

However, it’s important to note that while fintech has made investing more accessible, it also comes with its own set of challenges. Cybersecurity risks, data privacy concerns, and the potential for impulsive investing decisions are areas that both investors and industry players need to be mindful of.

Furthermore, as per SEBI (Investment Advisers) Regulations, 2013, all financial advice must be given by registered investment advisors. Online platforms that provide automated recommendations must ensure they comply with these regulations.

Looking ahead, we can expect to see more innovations in areas like artificial intelligence for personalised investment advice, blockchain for transparent transactions, and maybe even virtual reality for immersive financial education. The key will be balancing innovation with investor protection and regulatory compliance.

The road ahead is bright, to say the least!

Frequently Asked Questions

What is the role of fintech in mutual funds?

Fintech has allowed the growth of mutual funds to amplify and reach new heights. The sheer convenience that fintech brings to mutual fund investments has allowed thousands of new investors to enter the space and invest their savings.

How does fintech affect financial services?

The main advantage of fintech is that it has brought financial services to the larger masses. There is no gatekeeping in terms of complicated onboarding processes, lengthy documentation, or even any requirement to go down to the actual office. No matter where you are and what you’re doing, you’ll be able to access basic to intermediate financial services, all thanks to fintech.

How does fintech affect traditional financial institutions?

The rise of fintech has brought about a change in traditional financial institutions and the way we view financial services in general. The focus has shifted to making the process seamless and convenient for all investors.