We all know that there isn’t any such thing as a free lunch. But that still doesn’t stop us from hoping, does it?

Walking out of a restaurant without actually paying is going too far, of course. But when it comes to passive investing, it’s all fair game (minus the 1% or regulatory expenses charged, of course)!

It comes as no surprise that more and more Indian investors are now opting for mutual funds and ETFs over actively managed portfolios. This is on the basis of the data suggested below:

Growth of ETFs and Mutual Funds:

ETFs AUM Growth:

- 2014: Rs 351 crores

- 2024: Rs 6,27,244 crores

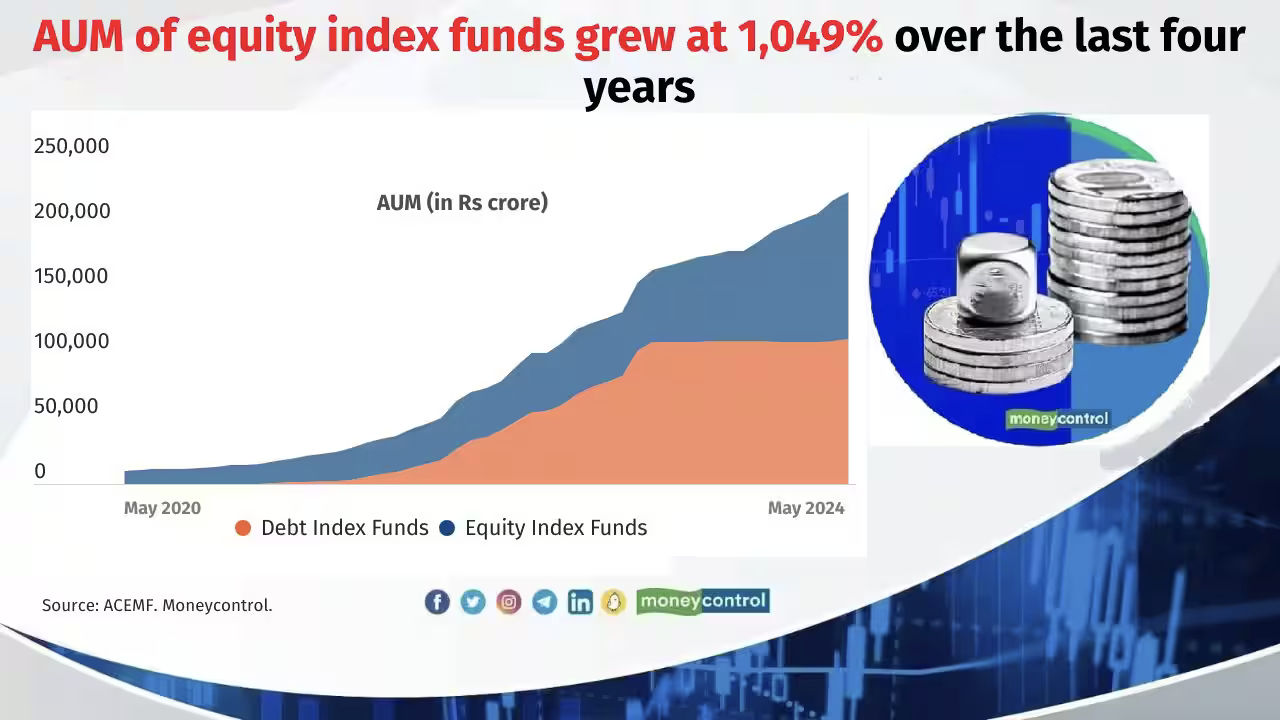

Index Funds Growth (Last Four Years):

- Growth Rate: 2,131%

- Current AUM: Rs 2.3 lakh crores

Source: MoneyControl

So, what is it about passive investing that attracts us?

Is it simply the fact that they’re more cost-effective than their actively managed counterparts?

Or is there more to the story?

Let’s find out!

What is Passive Investing?

Don’t worry, this isn’t going to be a long-drawn-out explanation that bores you.

Passive investing schemes focus on tracking or replicating the performance of an index. But not just any index, it tracks the one against which it is benchmarked.

To put it in simple terms, we can say – instead of spending time and effort in actively buying and selling shares, the fund manager attempts to replicate the performance of an existing portfolio or basket of stocks.

Let’s take a Nifty 50 index fund, for example.

Instead of selecting a single stock in the Nifty 50 index, the fund mirrors the entire composition of the index itself.

What does this mean?

The Nifty 50 comprises fifty companies based on free-float market cap. Your investment amount gets distributed among all these companies. If the index does well, so will your investment. And on the flip side, if the index underperforms, your investment will reflect that.

Now, this means that instead of putting all your hopes on one stock, your investment gets diversified across all the constituents of the Nifty 50 index.

ETFs, too, are very similar, albeit with one key difference — they trade on stock exchanges like individual stocks. ETFs, and Funds of Funds, along with index funds, are prime examples of passive mutual funds.

At the other end of the spectrum lies active investing. As you can imagine, the fund manager actively researches the markets and selects stocks. The aim, of course, is to create a portfolio where the stocks will appreciate in price shortly.

In an actively managed portfolio, fund managers aim to outperform the benchmark index. The higher the outperformance, the better it is, isn’t it?

The Shift Towards Passive Investing in India

Now, the debate on active vs. passive funds is centred around one key question: Is it worth it?

Let me explain.

As you can imagine, active funds come with a higher price tag. It involves the active buying and selling of securities.

As per Regulation 52 of the SEBI Mutual Fund Regulations, 1996, the expense ratio for actively managed schemes is higher than that for passive schemes.

Active funds aim to generate alpha, which helps them outperform the market benchmarks and averages. But this is where the debate gets interesting.

According to the 2023 S&P Indices Versus Active Funds (SPIVA) India, active funds have reportedly underwhelmed in their performance.

“Five out of ten large-cap funds underperformed the S&P BSE 100, while over 73% of mid- and small-cap schemes lagged the S&P BSE 400 MidSmallCap in 2023.” — Economic Times

Based on this data, it is safe to infer that passive schemes are becoming more viable and investable.

What’s Driving the Popularity of Passive Funds?

It is a combination of technological advancements and an increase in financial literacy.

The increased participation in passive funds is not just a result of investors switching from active to passive. Rather, it is also due, in a significant manner, to the entry of new retail investors into the Indian capital markets.

The investor awareness programs conducted by SEBI and AMFI have also played a major role in spreading awareness. Think back to all of AMFI’s Mutual Fund Sahi Hai campaign. They’ve been instrumental in educating the masses about investments in financial markets, specifically in mutual funds. The NSE and BSE investor awareness emails you keep getting all the time also serve an ulterior purpose.

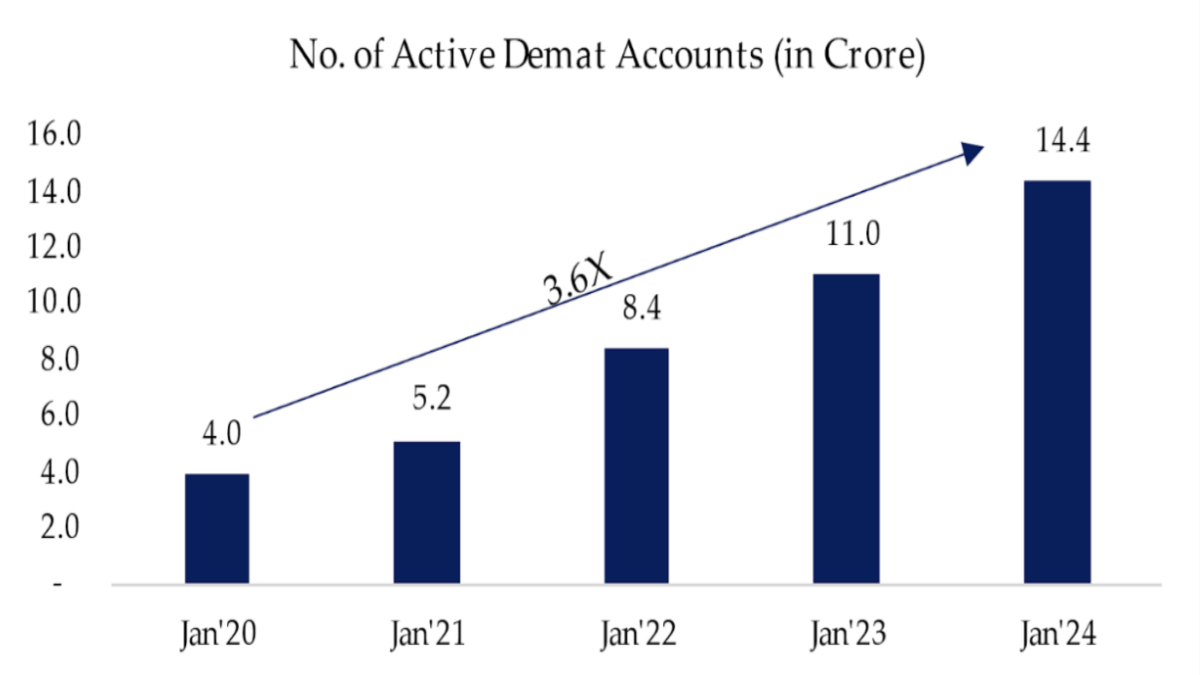

According to a Financial Express article dated February 25, 2024, between 2020 and 2024 alone, the number of Demat accounts in the country increased from 4 crores to 14 crores! That means about 10 crore new investors have joined the capital markets.

Source: FinancialExpress

Now, some of them will, of course, go for active management. Some may even try their hands at derivatives and the lot. Please be aware that derivative investments are highly risky. You should definitely understand your risk capacity before starting.

Some will try out passive investing through index funds and ETFs at some point.

It’s the only logical thing to do, after all.

Even if you believe in active investing, you’re going to create a diversified portfolio in the long run. Some portion of this portfolio will be allocated to passive funds.

“It is imperative to have the right mix of largely active funds with smaller amounts in passive funds.” — Economic Times as of April 08, 2024

The new-age retail investor is an enlightened investor. They are aware of the risks that come with being greedy in the stock markets. They prefer to be more proactive and sensible with their investment approach. They are also aware of how time-consuming active investment can be.

Investments in passive mutual funds like index funds, especially through SIPs, can be a game-changer. It helps inculcate a consistent and sustained approach to investing, especially for the long term.

It’s Not All Rosy

If you’re thinking of opting for passive investing, there are some drawbacks that you should be aware of.

- No Flexibility

Passive investing focuses on a portfoliol. You can definitely check what’s included in the portfolio, but you can’t specifically invest in a single stock directly depending on the market trends

For example, if you’ve invested in a Nifty 50 index fund, and there is currently a rally in power stocks, you won’t be able to alter the portfolio allocation. Similarly, if there’s a financial crisis or the stock market is going through a downturn, you won’t be able to shift away to investable stocks and weather the storm.

- Dependent on the Benchmark

Your portfolio returns are tied intricately to the performance of the chosen benchmark. If that particular benchmark underperforms your portfolio shall also replicate the same.

- Tracking Errors

The objective, of course, is to mirror the performance of the index. However, tracking errors can creep in and cause discrepancies in performance.

As the name suggests, tracking errors refer to any differences between the fund portfolio’s performance and the benchmark it mirrors.

This deviation can be caused by a number of factors. For instance, the fund’s expenses may impact the underlying securities, or the securities may breach their upper or lower circuits. Corporate action or any rounding off of the shares underlying the index may also have an effect.

What’s the Future Outlook?

We still have a very long way to go.

In spite of the phenomenal growth in mutual funds, especially the passive ones, we have barely scratched the surface. Data from RBI has shown that mutual fund investments only made up about 13% of total household financial assets in FY23.

That is dismal, to say the least.

But it also shows what the potential is.

Imagine if we could encourage more and more investors to participate in these funds. The Asset Under Management (AUM) would increase. There would be more inflows into the market. The demand and supply for goods would rise, individuals would have more income at their disposal and create jobs.

It’s all about mobilising funds — seeking to get the most utility out of our surplus. Your money is not going to do anyone any good if you keep it under your pillow, or in your bank account.

If you invest your money, however, you’re directly contributing to the growth and production of output. It’s a positive sum game — we all come out of it better! Having said that, of course, we recommend that you should definitely consult with your financial advisor before investing.

Frequently Asked Questions

Why is passive investing becoming more popular?

One of the main reasons why passive investing is becoming so popular in India is the sheer convenience it has started offering. Along with that is the knowledge and awareness that we are gaining. Anyone can start investing from anywhere, and it is more cost-effective as compared to active investing.

What are some of the issues related to the rise of passive investing?

One of the issues is the fact that you don’t get any chance to capitalise on short-term trends that may seek to beat the market. Instead, passive investing focuses on mirroring the market index and seeking potential returns.

What is a passive fund in India?

Passive funds in India focus on tracking the performance of a particular index. For instance, if we have a passive mutual fund, the fund portfolio will mirror the composition of the index.

Disclaimer:

Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Mutual Fund distribution services are offered through Dezerv Distribution Services Private Limited, a wholly owned subsidiary of Dezerv Investments Private Limited (collectively referred to as “Dezerv”) with AMFI Registration No.: ARN- 248439.

The information contained in this article is for knowledge purposes only. This article should not be construed to be an offer to buy/sell any securities or provide any investment advice to any party. Please refer to the Scheme Information Document, Key Investment Memorandum, Statement of Additional Information, risk-o-meter, client agreement, and other related documents for mutual fund schemes including specific risk factors provided therein.

In the preparation of this article, Dezerv has used information developed in-house and publicly available information and other sources believed to be reliable. While reasonable care has been made to present reliable data in this article, Dezerv does not guarantee the accuracy or completeness of the data. The information/data herein alone is not sufficient and shouldn’t be used for the development or implementation of an investment strategy. Actual results may differ from expressed or implied performance due to market uncertainties. The statements made herein may include statements of future expectations and other forward-looking statements that are based on our current views and assumptions.

This document should not be reproduced or redistributed to any other person without the prior permission of Dezerv.

Dezerv and/or its subsidiary/associates/employees are not liable for any risks/losses pertaining to any assets/securities or investment opportunities available from time to time.

External advice: Please consult your legal, tax and financial advisors to determine the implications or consequences of your investments in such mutual fund schemes or before making any investment decisions.